Risk Management Advisory & Governance Support

Our experience and expertise to the service of your Risk Management framework

Through the essence of their activities, the BMA team gets permanent exposure to the changing regulations and to all issues related to risk management, for all types of funds and financial institutions. First-hand experience includes a number of CSSF-agreed mandates as Directors, Conducting Officers in charge of Risk Management and Risk Managers.

BMA leverages on its experience and expertise in quantitative risk analysis, and in economic and financial analysis, to offer cutting-edge solutions to their clients in all aspects of pricing, risk management and risk-related regulatory requirements.

BMA has first-hand experience of designing and implementing risk models, especially VaR and stress-tests for market risk, as well as liquidity and credit risk modelling. Indeed, BMA has developed a proprietary analytics pricing and risk system (BMAnalytics) with dedicated models and metrics (incl. VaR, stress-tests) for equity, fixed-income and credit instruments.

BMA has also successfully performed several independent validation mandates for market, liquidity and credit risk models.

Market risk and VaR models validation

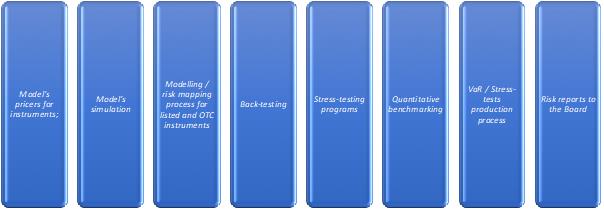

BMA perform independent validations of market risk models used for the monitoring of the global exposure of funds under management with the VaR / stress-tests approach.

We focus on

- the effective implementation of Management Companies risk models,

- the validation of the adequacy of VaR calculations,

- the validation of stress-tests simulations for strategies and instruments in the funds,

- checking compliance with the French AMF Règlement Général and CSSF Circulars 11/512 and 18/698.

Our independent validation cover all aspects

Our approach combines quantitative and qualitative analysis to provide a complete and detailed system / process review.

In particular, we propose to quantitatively benchmark the VaR/ Stress-tests produced by the Management Company against our own VaR system for samples of representative strategies.

Quantitative models validation & Risk Management Process design and implementation

BMA approach is to deliver concrete and practical solutions, and to go beyond mainstream consulting practices. To achieve this, BMA makes efficient use of its proprietary analytics library (BMAnalytics) which enables us to provide concrete numerical examples, case studies and prototypes where appropriate and feasible.

Past projects experience include

- Validation of several CCP market and counterparty risk models

- Validation of swaptions volatility cube generation and pricing model

- Review, validation and enhancement of the CVA and xVA platform including treatment of collateral risk

- Development and implementation of liquidity risk management frameworks for investment funds

- Development and implementation of regulatory stress test frameworks for Money Market Funds

- Design and calculation of risks associated to Private Equity funds with complex waterfalls

- Daily oversight, including calculation of daily VaR and stress tests (using BMAnalytics) for portfolios of Corporate, Emerging Markets bonds, Leveraged Loans, etc.

BMA’s team, specialized in quantitative finance and applied mathematics, is perfectly suited to address any complex subject in quantitative finance, quantitative modelling and risk management.

Secondment of Risk Managers and consultants

The BMA team offers secondment and hands-on support to its clients Risk Management operational teams in designing and implementing their risk management frameworks..

BMA puts at the disposal of their clients Risk Analysts and Risk Managers .

With a recruitment strategy focusing on backgrounds specialized in quantitative finance and applied mathematics, BMA’s team is perfectly suited to tackle all complex subjects of quantitative finance, quantitative modelling and risk management.

BMA’s Risk Managers provide support at all stages of the life cycle of funds and management companies (non-exhaustive list):

- Identifying, assessing and controlling the risks to which the investment funds are exposed:

- Defining investment funds risk profiles,

- Implementing specific risk management procedures,

- Implementing / performing new controls,

- Developing and implementing risk management systems,

- Risk limit monitoring, breach management and follow-up (analysis, communication, breach resolution follow-up, documentation), escalation process management,

- Updating and monitoring the various control dashboards,

- Enhancing the various reporting aimed at Chief Risk Officers, the Executive Committee and the Board of Directors,

- Undertaking the permanent Risk Management position for AIFM and UCITS management companies.

Training

BMA provides customized training to your risk management teams, sharing their deep hands-on knowledge of risk management techniques as well as extensive quantitative techniques, covering all pricing considerations, risk assessment and simulation techniques.

Dedicated professional training sessions are provided in French or English.

Please contact us for more details. We will review thoroughly your specific requirements to offer the most fitting training sessions to your teams.